Why Gross Margin Might Be Our Favorite Financial Metric

If you only had time to look at one number before deciding whether a business is worth your attention, what would it be?

Revenue? Too easy to inflate. Net profit? Too easy to manipulate. Growth rate? Tells you speed but nothing about quality. We'd pick gross margin.

Gross margin is the percentage of revenue left after you subtract the direct cost of delivering your product or service. If you sell a cup of coffee for 50 SEK and the beans, milk and cup cost you 15 SEK, your gross margin is 70%. That 70% is what's available to pay for everything else: rent, salaries, marketing, R&D, and (hopefully) profit.

The formula is simple:

Gross margin = (Revenue − Cost of Goods Sold) / Revenue

But the implications aren't simple at all.

What gross margin actually tells you

A high gross margin signals that the company creates a lot of perceived value relative to what it costs to produce. And that usually means one of two things: either the product is genuinely differentiated (branding, technology, switching costs), or the company has figured out how to produce at very low cost (scale economies, process power).

Gross margin is a proxy for moat strength.

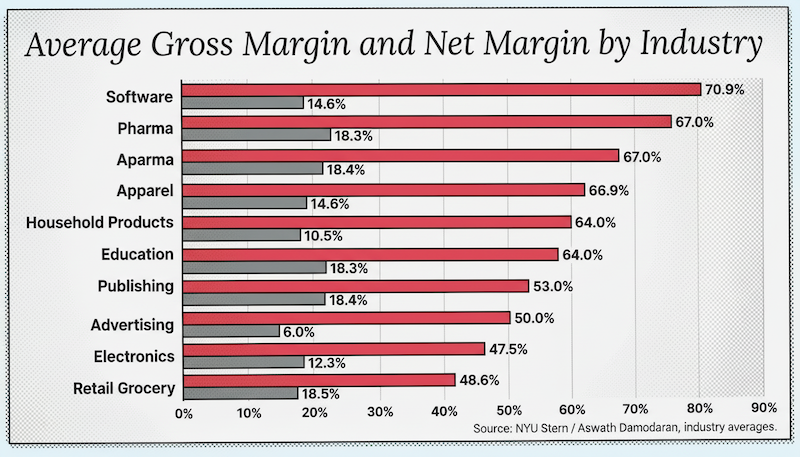

Look at the chart below and you'll see this pattern clearly.

The moat connection

Software sits at the top with a 70.9% gross margin. That shouldn't surprise anyone. Once you've built the code, the cost of serving one more customer is close to zero. This is operating leverage in its purest form, and it's one reason why software companies tend to command eye-watering valuations.

Pharma is right behind at 67.0%. The cost of manufacturing a pill is almost nothing. The value comes from the R&D and the patent protection (a cornered resource, in Hamilton Helmer's 7 Powers framework). As long as the patent holds, you've got pricing power. When it expires, generics flood in and the margin collapses. The moat has a timer on it.

Now compare that to retail grocery at 24.7%. Selling food is inherently a low-margin game. The products are commoditized, switching costs are near zero (your customers can walk to a competitor in 5 minutes), and supplier bargaining power is real. If you run Porter's Five Forces on a grocery chain, almost every force works against you.

The gap between 70.9% and 24.7% is the gap between a business that can invest aggressively in growth and one that's fighting for every percentage point.

The gap between gross and net

Note that a high gross margin doesn't automatically mean high profits.

Software has a 70.9% gross margin but "only" 14.6% net margin. Where did the other 56 percentage points go? R&D, sales teams, cloud infrastructure, stock-based compensation. Software companies tend to reinvest heavily because the economics allow it. When your gross margin is 71%, you can afford to spend a lot on growth and still have something left.

Pharma tells a similar story: 67% gross, 18.4% net. The difference is mostly R&D (finding the next blockbuster drug is expensive) and regulatory compliance.

Entertainment is the cautionary tale: 40.4% gross but only 0.9% net. The cost of the content itself isn't terrible, but the overhead of running a studio, marketing campaigns, and the sheer unpredictability of hits vs. flops eats almost everything.

And then there's apparel: 51.8% gross margin (surprisingly high!) but 5.1% net. The raw materials are cheap, but the marketing, retail presence and inventory risk swallow the rest. You're paying for the brand, which is exactly why branding is one of the 7 Powers.

When high margins attract predators

Jeff Bezos once said "Your margin is my opportunity." It's one of the most quoted lines in business strategy, and right now it's playing out in real time against the software industry.

Software sits at the top of our chart with a 70.9% gross margin. For two decades, that margin fueled a golden era. SaaS companies built sticky subscription models, compounded recurring revenue, and commanded premium valuations. A typical enterprise SaaS company traded at 10-15x revenue. The logic was simple: high gross margins, predictable cash flows, low churn. What's not to like?

Then AI showed up and said: I can do some of that too.

In the four months leading into February 2026, the software sector's forward P/E ratio dropped from roughly 39x to 21x, the largest valuation compression since the 2002 dot-com bust. Between mid-January and mid-February alone, roughly one trillion dollars was wiped from the collective value of software stocks. Adobe, Salesforce, ServiceNow: all down 25-30% year-to-date, even as they reported strong results.

The trigger? A series of AI product launches demonstrated that autonomous agents can now handle complex knowledge work. The market's reaction was blunt: if AI agents can replicate what enterprise software does, then those fat margins are up for grabs.

This is Bezos's line made real. A 70% gross margin is a wonderful thing when your moat holds. But it's also a giant neon sign saying "there's a lot of value here that someone else might capture." AI poses a structural threat to seat-based licensing models, and some vendors are already seeing slower seat growth as customers become more efficient. Instead of 500 licenses, a company buys 450 and lets an AI agent handle the rest. That doesn't kill the business. But it compresses the margin.

The interesting question is whether the panic is justified. Salesforce CEO Marc Benioff called the notion that software will be replaced by AI "the most illogical thing in the world." Gartner still projects worldwide software spending to grow 14.7% in 2026 to over $1.4 trillion. The companies with real moats (deep enterprise integration, proprietary data, regulatory lock-in) will probably be fine. The ones coasting on inertia and switching costs alone? Those are the ones Bezos was talking about.

There's a lesson here that goes beyond software stocks. High gross margins attract competition. Always. The only question is how long your moat can hold them off. Porter's Five Forces tells you where the pressure comes from. Helmer's 7 Powers tells you what kind of defenses work. And the market, eventually, tells you if you were right.

Why this matters for your career

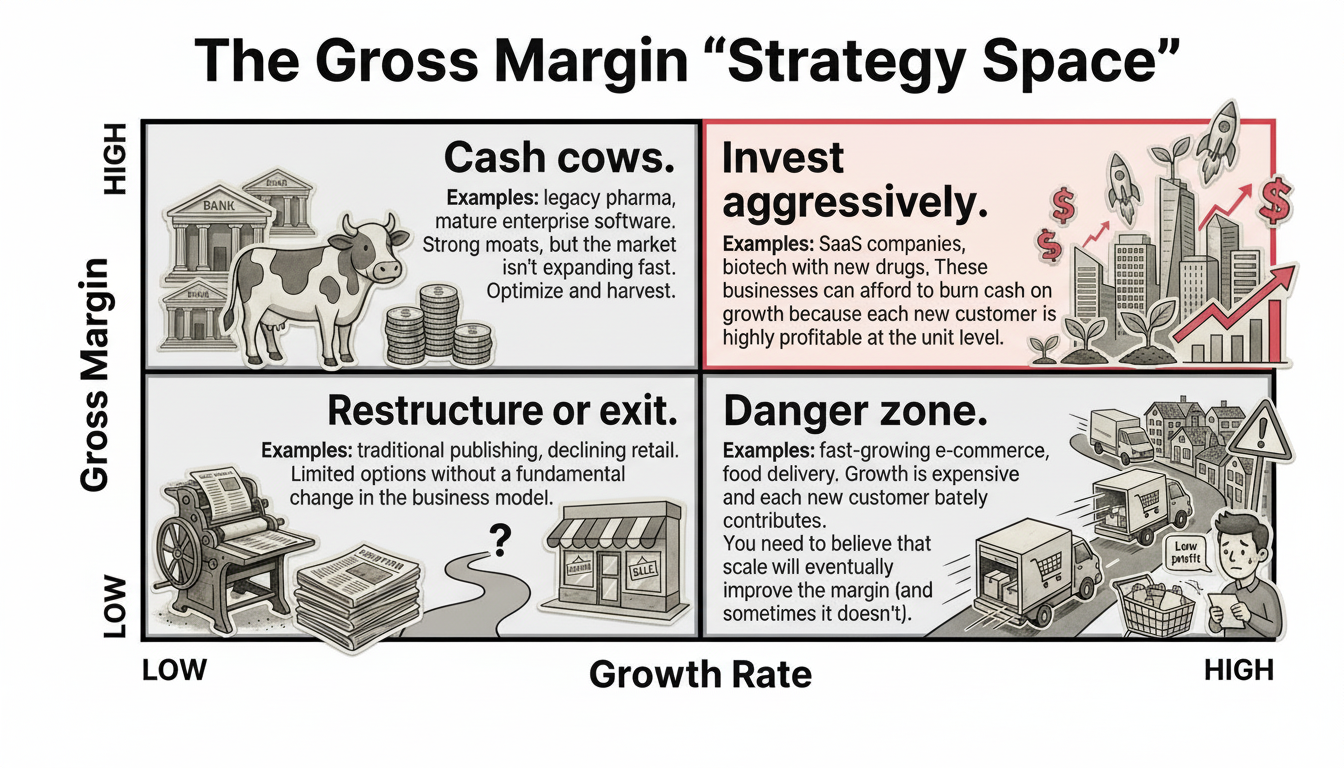

If you work in a high gross margin industry, your company has options. It can invest in product, hire ahead of demand, experiment with new markets, and absorb mistakes. If you work in a low gross margin industry, every decision is tighter. There's less room for error, less budget for experiments, and more pressure on operational efficiency.

This doesn't mean low-margin businesses are bad. IKEA, Costco and Walmart are extraordinary companies. But they win through scale economies and process power, not through pricing power. They've built moats on the cost side, not the value side.

Knowing where your company sits on this spectrum changes how you think about strategy, hiring, pricing, and growth.

Now there's a flip side to this as well: if you're an entrepreneur or intrapreneur looking for your next move, the same chart above could be a treasure map.

Industries with fat gross margins are telling you something: there is a lot of value being created here, and customers are willing to pay for it. That might be exactly where you want to build. Not because you'll enjoy those margins forever, but because high-margin spaces give you room to experiment, iterate and survive your early mistakes. A startup burning cash in a 70% gross margin industry has a fundamentally different runway than one fighting for scraps at 25%.

Think about it this way: every percentage point of gross margin is a percentage point you can reinvest in product quality, customer experience, or simply in buying yourself more time to find product-market fit. The best founders instinctively gravitate toward industries where the unit economics are generous enough to absorb the inevitable stumbles of building something new.

So the next time you're scanning for business ideas, pull up gross margin data by industry and ask: where are the fat margins, and what would it take to earn a slice? The answer might be more accessible than you think.

When we teach strategy and business models in the Pareto MBA, gross margin is one of the first things we look at. Before you analyze the org chart, the sales funnel or the competitive landscape, ask one question: how much does this company keep on every unit sold?

The answer might tell you more than a 50-page strategy deck.

Gross margin analysis is one of many practical frameworks we cover in the Pareto MBA, an 8-week program for professionals who want to build real business acumen without going back to university. Not sure yet? Start with MBA Essentials, our free 8-part email course.