The 80/20 of Nvidia: What the World's Most Valuable Company Can Teach You About Reading Financial Statements

A mini crash course in business analysis, using the company at the center of the AI revolution.

Nvidia is the most valuable company in the world by market capitalization. At roughly $4.5 trillion, it's worth more than the entire stock markets of most countries. But what does Nvidia actually do? How do you read the financial statements that tell the story of a company this successful? And how do you figure out whether it can keep going?

This article is a mini crash course in business analysis, using Nvidia as our case study. We'll cover the basics of financial statements, how to spot a moat, how to think about value chains, and some of the risks hiding beneath the surface. It's the kind of analysis we teach in the Pareto MBA, applied to the company at the center of the AI revolution.

Let's start with the business itself.

What does Nvidia actually do?

Nvidia designs chips. That's the short version.

The longer version: Nvidia is a "fabless" semiconductor company, which means they design chips (GPUs, specifically) but don't manufacture them. The actual manufacturing is done by TSMC, a Taiwanese company that runs the world's most advanced chip foundries.

This is an important distinction. Companies like Intel have historically done both: designed chips and manufactured them in their own factories. Nvidia chose a different path. They focused entirely on design and intellectual property, and outsourced the physical production.

That choice turned out to be spectacularly right. Nvidia's GPUs, originally built for rendering video game graphics, turned out to be perfectly suited for training AI models. When the AI boom hit, Nvidia had the best product and the deepest ecosystem. Every major AI lab, cloud provider and tech giant needed their chips. Badly.

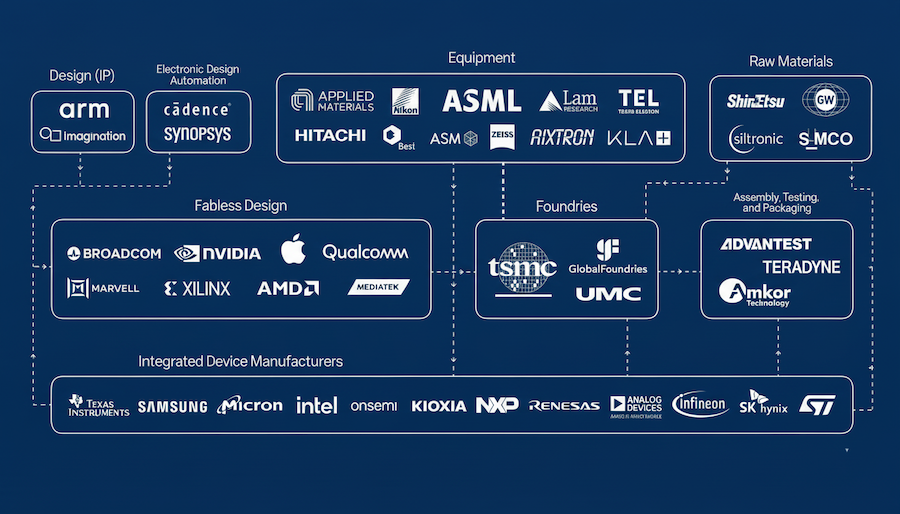

Understanding the semiconductor value chain

Before we look at the financials, it helps to understand where Nvidia sits in the semiconductor ecosystem.

Think of the chip industry as a chain with several links: Design IP (companies like ARM and Synopsys provide the foundational building blocks), Electronic Design Automation (Cadence and Synopsys provide the software tools used to design chips), Fabless Design (this is where Nvidia sits, alongside Apple, AMD, Broadcom and Qualcomm: they design the chip but don't make it), Foundries (TSMC, Samsung and GlobalFoundries actually manufacture the chips), Equipment (ASML, Applied Materials, Lam Research: they build the machines that the foundries use), Raw Materials (Shin-Etsu, Siltronic: the silicon and other materials), and Assembly, Testing and Packaging (Amkor, Advantest: the final steps before a chip ships).

At the bottom of the chain you also have Integrated Device Manufacturers like Intel, Samsung and Texas Instruments, who do multiple steps themselves.

The key takeaway here is that Nvidia is deeply dependent on other players, especially TSMC. According to publicly available data, TSMC accounts for about 43% of Nvidia's supply chain. But interestingly, Nvidia only represents about 6.3% of TSMC's revenue. That's an asymmetric dependency, and it matters when you're thinking about risks and negotiating power.

Nvidia clearly understands this. They recently took a $2 billion stake in Synopsys, one of the key EDA companies upstream of them. They also tried (and failed) to acquire ARM for $40 billion, which would have given them control over the design IP layer. Jensen Huang, Nvidia's CEO, is playing the long game in this value chain.

The three financial statements (a quick primer)

If you're new to financial statements, there are really only three you need to know. Together, they tell the story of a company's health.

The Income Statement shows how profitable a company has been over a period of time (say, one year). It starts with revenue at the top, then subtracts various costs and expenses until you arrive at net income at the bottom. Think of it as a movie: it shows what happened over a stretch of time.

The Balance Sheet shows what a company owns (assets), what it owes (liabilities) and what's left for shareholders (equity) at a specific point in time. It's a snapshot, like a photograph. And it always balances: assets = liabilities + equity.

The Cash Flow Statement shows how the company's cash position changed during the period. This is important because the income statement can include things that aren't actual cash (like depreciation), while the cash flow statement shows you the real money moving in and out.

These three statements are connected. The balance sheet at the start of the year, combined with the income statement and cash flow statement for the year, give you the balance sheet at the end of the year.

Now let's apply this to Nvidia.

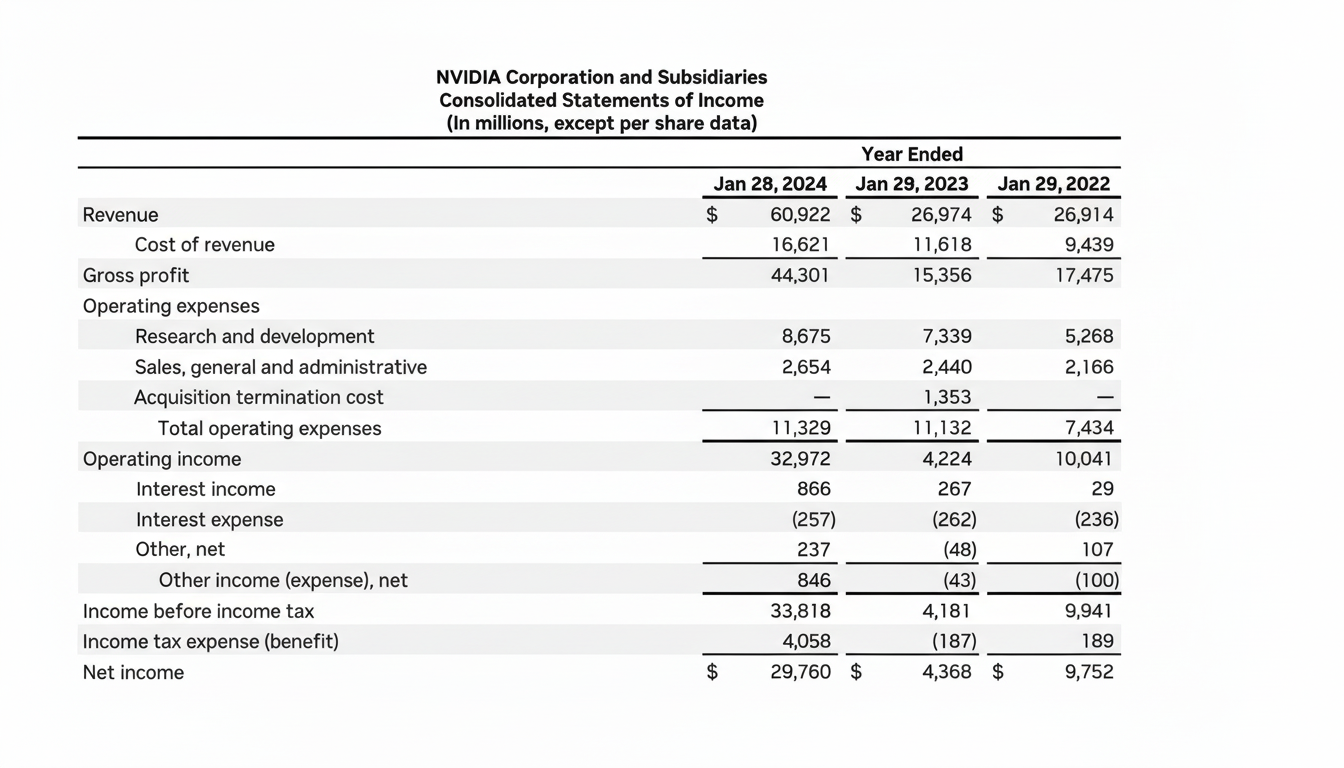

Reading Nvidia's income statement

Here are the things that jump out:

Revenue doubled. From about $27 billion in fiscal year 2023 to about $61 billion in fiscal year 2024. That's 126% growth in a single year. For a company of this size, that's extraordinary. (And by fiscal 2025, revenue had doubled again to $130.5 billion.)

Gross profit is enormous. In fiscal 2024, gross profit was $44.3 billion on $60.9 billion in revenue. That's a gross margin of about 73%. By fiscal 2025, it climbed to 75%. A gross margin this high tells you that the cost of making each dollar of revenue is very low relative to what they can charge. This is a sign of pricing power.

Operating expenses are well controlled. R&D was $8.7 billion and SG&A was $2.7 billion. Notice that R&D is more than 3x the size of sales costs. Nvidia is a company that invests heavily in staying ahead technically.

Net income went from $4.4 billion to $29.8 billion in one year. That's a 580% increase. The combination of explosive revenue growth with expanding margins (not shrinking ones) is extremely rare and a once in a generation thing.

One practical tip when reading income statements: always look at the trend, not just one year.

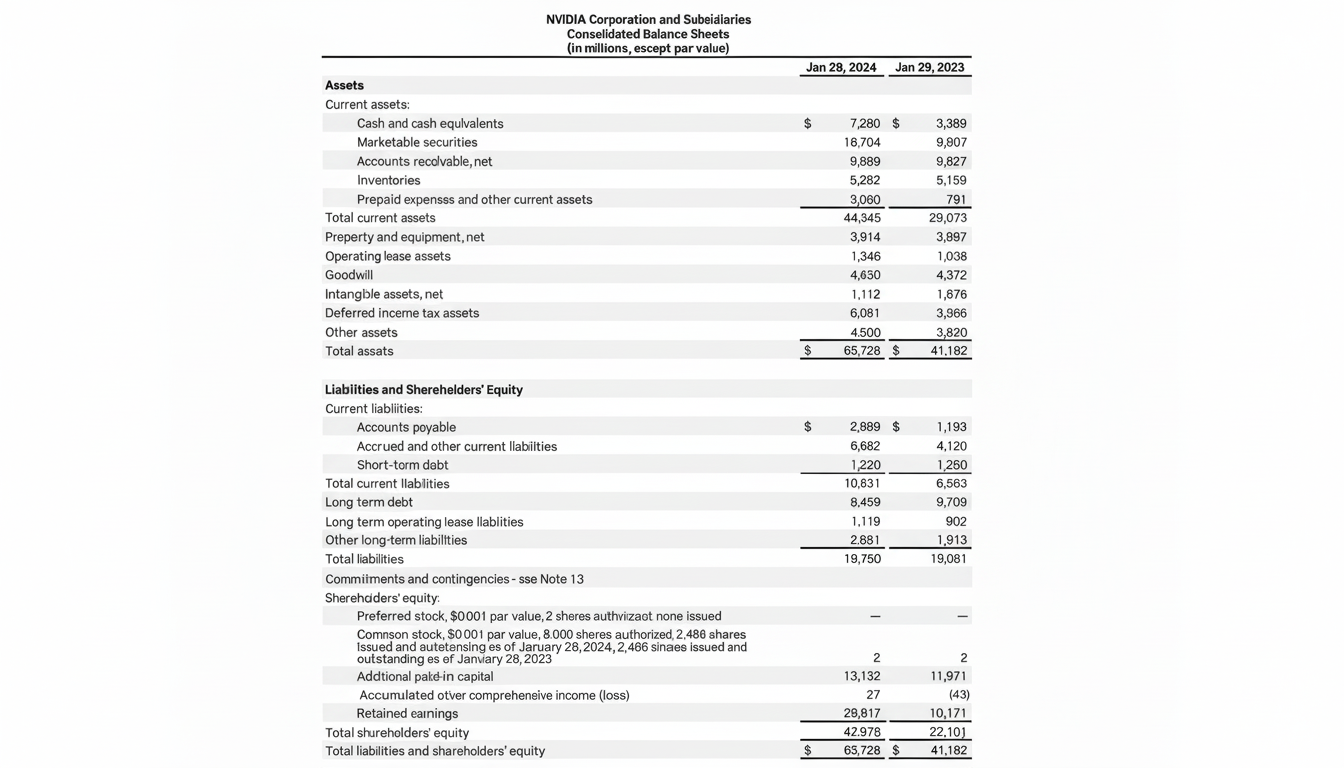

Reading Nvidia's balance sheet

Total assets grew from $41 billion to $66 billion in one year. Where did the growth come from? Mostly current assets, which nearly doubled from $23 billion to $44 billion. Cash and marketable securities alone went from $13.3 billion to $26 billion. The company is swimming in cash.

Accounts receivable jumped from $3.8 billion to $10 billion. This means customers owed Nvidia a lot more money at the end of the year. That's normal when revenue doubles, but it's worth keeping an eye on. If receivables grow faster than revenue, that can sometimes be a warning sign.

Goodwill barely changed ($4.4 billion both years), which tells you Nvidia's growth was organic, not driven by acquisitions.

On the liabilities side, total debt was about $9.7 billion. Compare that to cash of $26 billion. Nvidia has net cash of around $16 billion. They could pay off all their debt tomorrow and still have billions left over.

Retained earnings tripled from $10.2 billion to $29.8 billion. A balance sheet this clean, with this much cash and this little debt relative to equity, gives a company enormous strategic flexibility.

How to spot a moat

So Nvidia has incredible numbers. But the numbers are just the scoreboard. The interesting question is: why are the numbers so good? And can they stay that way?

Warren Buffett popularized the concept of a "moat": a sustainable competitive advantage that protects a company from competition, like the moat around a medieval castle.

There are several frameworks for thinking about moats. Two that we use in the Pareto MBA:

Porter's Five Forces looks at the factors working against you: the bargaining power of your suppliers and customers, the threat of new entrants and substitutes, and the intensity of rivalry in your industry.

Hamilton Helmer's Seven Powers describes seven types of moats: Scale Economies, Process Power, Counter-positioning, Cornered Resources, Network Economies, Switching Costs and Branding.

Porter's Five Forces applied to Nvidia

Bargaining power of suppliers: High. Nvidia depends on TSMC for manufacturing. There's no easy alternative at the cutting edge. If TSMC raises prices or prioritizes other customers, Nvidia has limited options.

Bargaining power of customers: Moderate but growing. Nvidia's biggest customers are hyperscalers like Microsoft, Google, Amazon and Meta. These companies are massive, and they're all developing their own chips. For now, Nvidia's products are significantly better, which limits customer leverage. But as alternatives improve, this could shift.

Threat of new entrants: Low in the short term. Designing a competitive GPU takes years of accumulated engineering knowledge, massive R&D spending, and a mature software ecosystem (CUDA is a huge part of their advantage).

Threat of substitutes: Moderate. The main substitute isn't a different chip; it's the question of whether demand for AI compute will keep growing at this pace. If AI models become much more efficient, demand could plateau.

Industry rivalry: AMD is the main competitor in GPUs, but Nvidia holds roughly 80%+ market share in data center GPUs. For now, rivalry is limited by Nvidia's technical lead, but this is the force most likely to intensify over time.

Helmer's Seven Powers applied to Nvidia

Switching Costs: Very strong. Nvidia's CUDA ecosystem is deeply integrated into the AI development workflow. Millions of developers, thousands of AI models, and countless libraries and tools are built on CUDA. Switching to AMD isn't just about buying a different chip; it means rewriting code, retraining models, and rebuilding workflows. This is probably Nvidia's deepest moat.

Cornered Resources: Strong. Nvidia has Jensen Huang (who has led the company for 30+ years), a world-class chip design team, and years of accumulated IP.

Scale Economies: Growing. The larger Nvidia gets, the more it can invest in R&D while spreading that cost across a massive revenue base. Nvidia spent $8.7 billion on R&D in fiscal 2024. Most competitors can't match that.

Branding: Moderate. In enterprise tech, Nvidia has become synonymous with AI compute. That's valuable, but it's more of a B2B brand advantage than a consumer one.

Network Economies: Moderate. The more developers use CUDA, the more tools get built, the more attractive the platform becomes. There's a flywheel here, but it's not as strong as a pure consumer network effect.

The risks hiding beneath the surface

Nvidia's numbers look phenomenal. But there are real risks, and understanding them is just as important as understanding the moat.

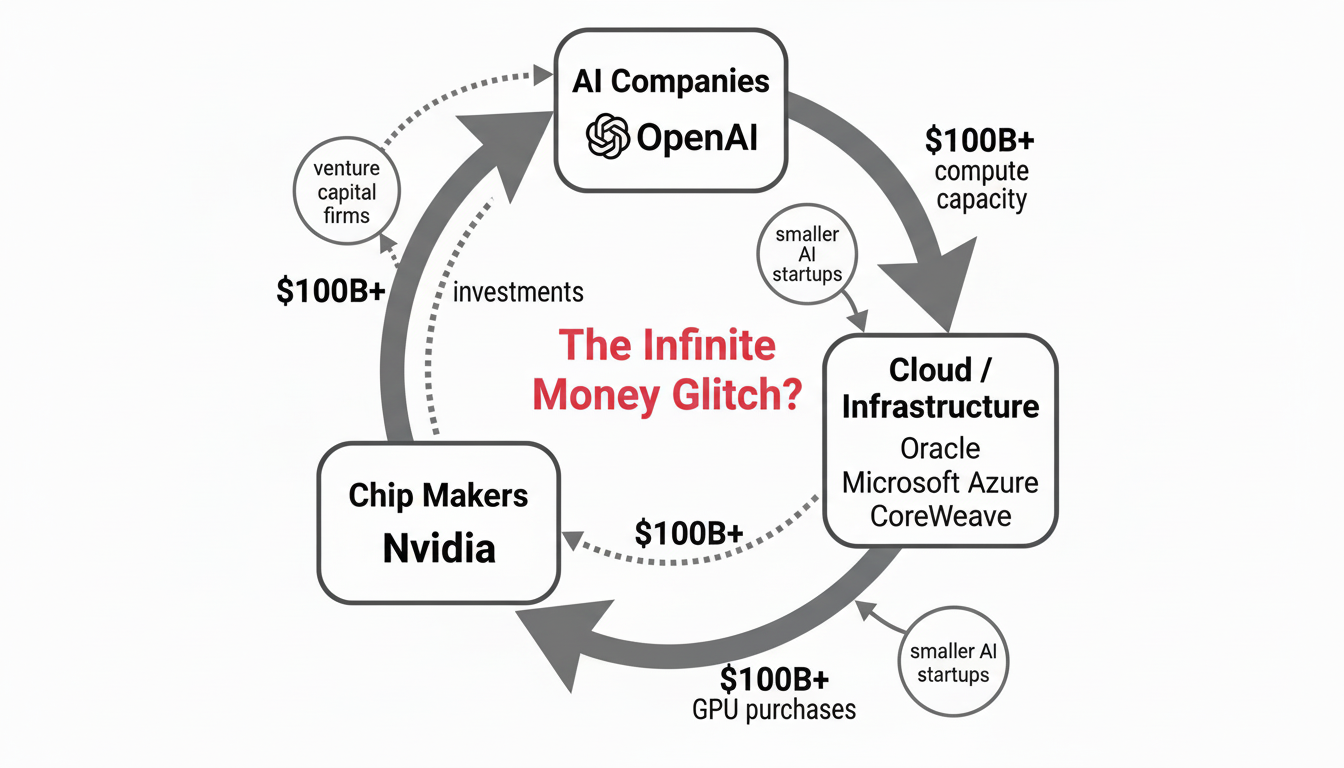

Circular financing in the AI ecosystem. This is probably the most intellectually interesting risk. Look at how money flows: Microsoft invests in OpenAI. OpenAI buys compute from Microsoft Azure. Azure buys Nvidia GPUs. Nvidia invests in OpenAI. OpenAI signs a $300 billion deal with Oracle for data center capacity. Oracle spends billions on Nvidia chips.

Do you see the circularity? There's a risk that some portion of the money flowing through this system is being recycled rather than representing genuinely independent demand.

Commoditization vs. Jevons Paradox. As AI chips get cheaper and more efficient, will that kill Nvidia's margins? Or will it do the opposite: make compute so affordable that demand explodes? Historically, when technology gets cheaper, demand increases faster than prices fall (this is the Jevons Paradox, first observed with coal consumption in the 1800s). But past performance doesn't guarantee future results.

Geopolitical risk. TSMC manufactures Nvidia's most advanced chips in Taiwan. The geopolitical situation between China and Taiwan is a genuine risk factor for the entire semiconductor supply chain.

Value chain squeeze. Is it enough to "just" design chips, or will companies that control more of the value chain ultimately win? Nvidia is more dependent on TSMC than TSMC is on Nvidia. That power imbalance is worth watching.

"Too interconnected to fail." So many large, important companies have a stake in Nvidia's continued success that there's a question of systemic risk. What happens if the AI investment cycle cools down?

A quick note on accounting tricks

Financial statements are supposed to give a fair representation of a company's health. But there's always some room for storytelling (as Warren Buffett once said: EBITDA is "bullshit earnings").

Some common tricks to watch out for: recognizing revenue too soon (booking revenue before the customer has committed), changes in activation practices (reclassifying R&D spending as an "investment" on the balance sheet), alternative metrics (the more adjustments to "adjusted EBITDA," the more suspicious you should be), and moving things off the balance sheet (what Enron did with special purpose vehicles).

We're not saying Nvidia is doing any of this. Their statements are audited under US GAAP. But the circular financing dynamics in the broader AI ecosystem do raise questions about how "real" some of the reported revenue actually is. It's worth being aware of.

Takeaways

If you've made it this far, here's what you should take away:

- Financial statements tell a story, but you need all three (income statement, balance sheet, cash flow statement) to get the full picture.

- Margins and growth are the first place to look for moats. A company that doubles revenue while expanding gross margins from 73% to 75% is doing something most companies can't.

- Value chains matter. Understanding where a company sits in its ecosystem is often more useful than memorizing financial ratios.

- Frameworks help structure your thinking. Porter's Five Forces and Helmer's Seven Powers give you a systematic way to assess competitive advantage.

- Risks aren't always in the financial statements. The circular financing dynamics, the geopolitical situation with Taiwan, the question of AI demand sustainability — none of these show up as line items.

- The best analysts combine business understanding with financial literacy. Learning to read the three main financial statements and connect them to competitive dynamics will make you a much sharper thinker.

Financial statement analysis, competitive moats, and value chain thinking are core frameworks we cover in the Pareto MBA, a program for professionals who want to build real business acumen without going back to university.