The Manager's Real Job: Capital Allocation

You probably didn't get promoted because of your budgeting skills. But now that you're in charge, the most important thing you do every day is decide where to put resources.

You probably didn't get promoted because of your budgeting skills. Maybe you were the best engineer, the top salesperson, or the person who always managed to keep a team running smoothly. But now that you're in charge, your job has quietly shifted. Whether you run a ten-person team or a thousand-person division, the most important thing you do every day is decide where to put resources. And where not to.

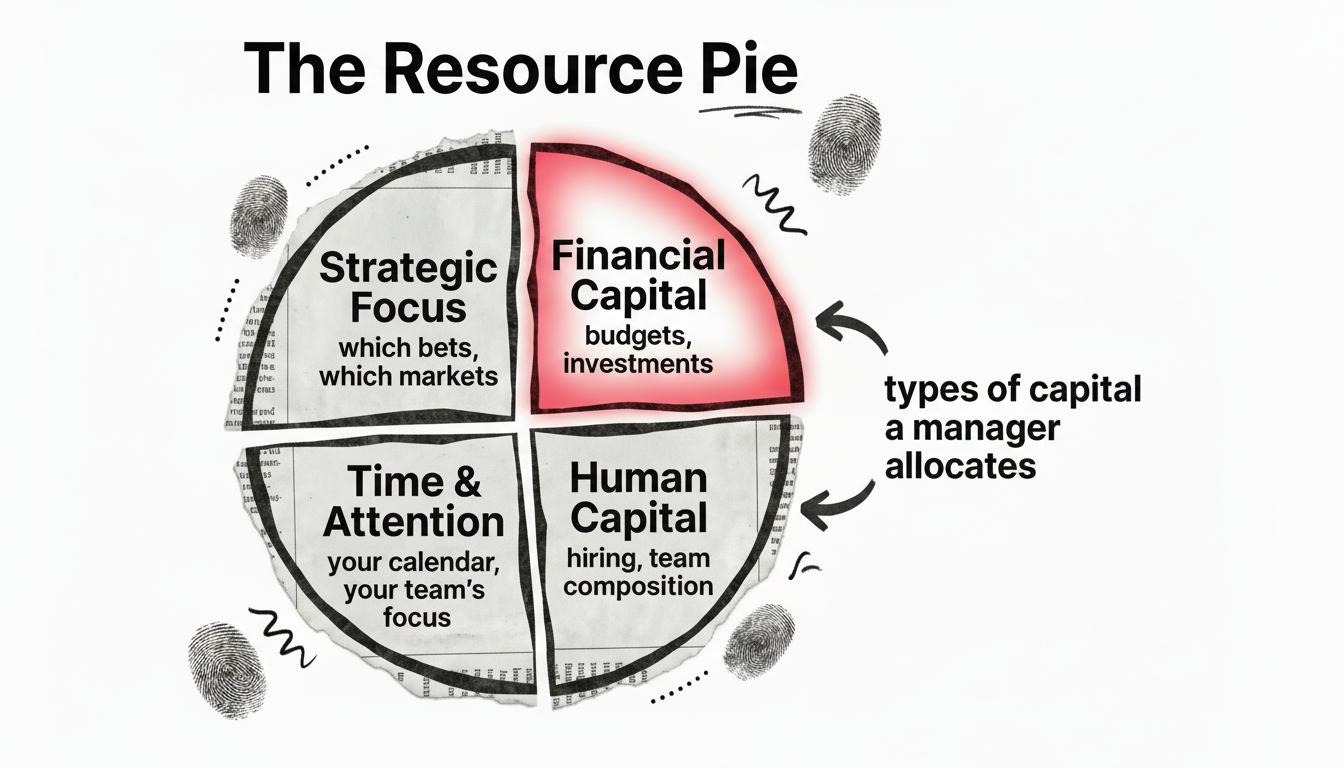

That's capital allocation. The term sounds like something from a finance textbook, but it's really just the practice of choosing how to use what you've got: money, people, time, and attention. Every "yes" to one thing is a "no" to something else. Every hire, every project, every meeting that fills up a calendar is an allocation decision. You're already making them. The question is whether you're making them deliberately.

Money decisions (the obvious ones)

Let's start where most people's minds go: the budget. When you decide to invest in a new piece of equipment, expand to a new market, or upgrade your software, you're allocating financial capital. These decisions tend to get the most scrutiny because they show up on spreadsheets. But they're only part of the picture.

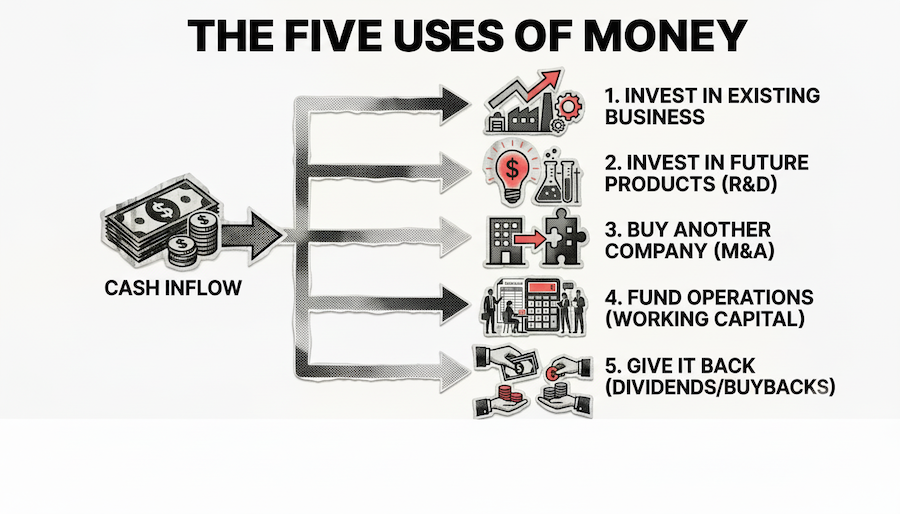

When you zoom out, there are really only five things a company can do with its money:

- Invest in the existing business. New equipment, better software, expanded production capacity. This is the most intuitive use of capital: spend money now to produce more or better output later.

- Invest in future products. Research and development is spending today to create the things you'll sell tomorrow. It's harder to measure than buying a machine, but for many companies it's the single most important allocation decision they make.

- Buy another company. Acquisitions let you grow faster than you could on your own, by picking up customers, technology, or talent in one move. The catch: most studies show that the majority of acquisitions fail to create value. The buyer tends to overpay, and the promised synergies turn out to be harder to realise than the PowerPoint suggested.

- Fund day-to-day operations. Working capital is the money tied up in inventory, unpaid invoices, and other short-term needs. It's not glamorous, but it's real. A growing company that makes a profit can still go bankrupt if it doesn't handle its cash flow. Growth binds capital, and it can take a surprisingly long time to get money back.

- Give it back. If you genuinely have more cash than good ideas, the honest thing to do is return it to the owners. This sounds like giving up, but it's actually a sign of discipline. The alternative, pouring money into mediocre projects just because it's there, is far worse.

Most managers spend the bulk of their energy on the first two. The great ones think across all five and are honest about which one makes the most sense at any given moment.

People decisions (the ones that actually keep you up at night)

This is where it gets interesting, because most managers don't think of hiring and team composition as allocation decisions. But they are, and they're often the most consequential ones you'll make.

When you choose to hire a second salesperson instead of a first data analyst, that's an allocation decision. When you promote someone into a leadership role, you're betting that they'll generate a return in the form of a better-functioning team. When you let someone go who isn't performing, you're freeing up a salary, a desk, and management attention for someone who might use those resources better.

Think about your own calendar for a moment. The people you spend time coaching, the teams you sit in on, the one-on-ones you prioritise. That's you allocating your scarcest resource: your own attention. If you're spending half your week in status meetings with a team that runs fine on its own, while a struggling team gets thirty minutes a month, that's a misallocation just as real as overspending on a bad project.

Time and focus decisions (the invisible ones)

Time is the resource nobody puts on a balance sheet, but it might be the most valuable one your company has. Every initiative competes for the same pool of hours and mental energy. When you launch a new strategic project, you're not just spending money. You're asking people to care about one more thing.

This is where many growing companies get into trouble. They keep adding priorities without removing any. The roadmap gets longer, the team gets stretched thinner, and suddenly everyone is busy but nothing moves forward with real momentum. The capital allocation lens helps here: what would happen if you killed three projects and focused all that time and talent on the one that actually matters most?

The same logic applies to your own time as a leader. Saying yes to a conference, a board seat, or a cross-functional initiative means saying no to something else, even if that "something else" is just unstructured time to think. Some of the best capital allocators in history were known for keeping their calendars remarkably empty, because they understood that strategic thinking requires space.

The decisions nobody wants to make

The hardest allocation decisions aren't about where to invest. They're about where to stop investing.

Shutting down a product line that a team has worked on for two years. Exiting a market that seemed promising but isn't paying off. Restructuring a department that used to be the company's engine but has become a drag. These decisions are painful because they involve real people and real emotions. A manager who built their career on a specific business unit will fight to keep it alive long past the point where the numbers justify it.

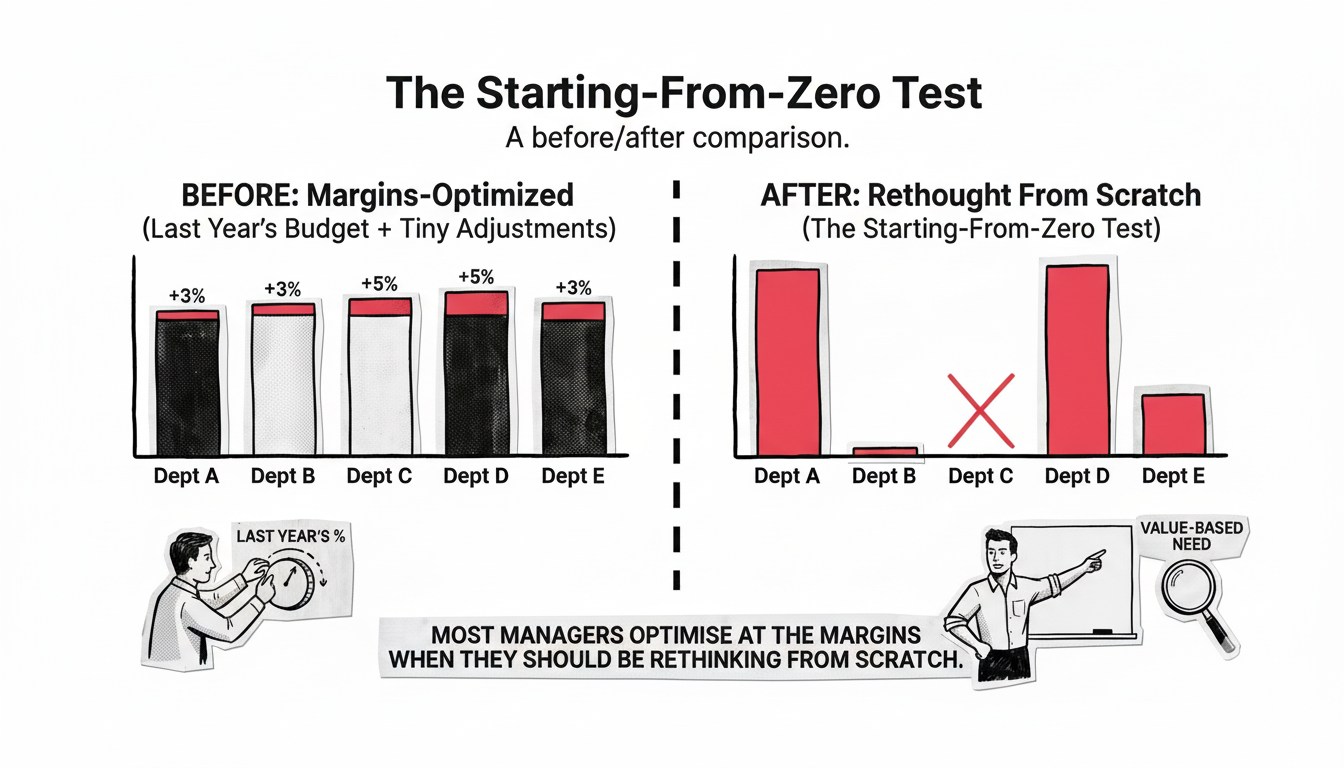

But keeping resources locked in something that isn't working has a real cost. Not just the money, but the opportunity cost of what those people, that budget, and that leadership attention could be doing elsewhere. Good capital allocators develop the habit of asking one deceptively simple question: "If I were starting from scratch today, would I invest in this?" If the answer is no, the right move is usually to stop, no matter how much has already been spent.

The traps

If this sounds straightforward in theory, it's worth understanding why it goes wrong in practice.

The most common trap is inertia. In most organisations, this year's budget looks suspiciously like last year's, plus or minus a few percent. Nobody asks whether the marketing team should still get the same share as it did three years ago, or whether the R&D budget reflects today's strategy or one that's already been abandoned. The budget becomes a political artefact rather than a strategic tool.

The second trap is imitation. There's enormous pressure to copy what competitors are doing, especially when it comes to trendy investments. If every company in your industry is pouring money into AI, it feels risky not to follow, even if you haven't figured out what AI would actually do for your specific business. Warren Buffett called this the "institutional imperative," and it's responsible for more wasted capital than almost anything else.

The third trap is refusing to quit. Humans are wired to protect past decisions. We'd rather spend another million trying to make a bad acquisition work than admit it was a mistake and move on. You've probably seen it in action. The antidote is simple but painful: ignore what you've already spent, and judge every investment on its future merits alone.

A different way to look at your job

Here's the shift we encourage in the Pareto MBA: start seeing yourself not just as a manager of people or products, but as a manager of resources. Every decision you make, from the annual budget to your Tuesday afternoon calendar, is an allocation decision. Some are big and visible. Others are small and invisible. But they all compound.

The managers who create the most value over time aren't necessarily the ones with the best ideas or the biggest budgets. They're the ones who consistently put resources where they'll do the most good, and have the courage to pull them back when they won't. That's capital allocation. And it might be the most important skill nobody taught you.

Capital allocation is one of many practical frameworks we cover in the Pareto MBA, a program for professionals who want to build real business acumen without going back to university.